Retirement Planning Made Simple

- Sean Kelleher

- 12 hours ago

- 9 min read

Contents:

A. Keeping it Simple

B. The Flow of Money: Income In, Benefits Out

C. The Stages of Retirement Planning

1. The Risk Period

2. Old Money vs. New Money

3. Pre-Retirement

4. Retirement

D. Summary: Simplicity Through Managing Complexity

Defining Risk Profiles: Defensive, Cautious, Balanced, Growth and Aggressive

Probability Analysis and Ongoing Management

"There seems to be some perverse human characteristic that likes to make easy things difficult." Warren Buffet.

A. Keeping it Simple

Retirement planning is often complicated by a simple fact: one solution does not fit everyone. Individuals have different incomes, currencies, investment horizons, attitudes towards risk, and retirement objectives. Add inflation, market cycles, and life expectancy into the equation, and retirement planning can appear overwhelming.

The purpose of this paper is to simplify the process by focusing on the key principles that underpin a successful retirement strategy. Whether seeking professional advice or managing investments independently, understanding these principles can help improve decision-making and long-term outcomes.

We define retirement planning as the process of preparing today for future financial independence, enabling an individual to continue meeting their lifestyle goals and aspirations throughout retirement. In essence, it is a long-term project that rewards discipline and consistency rather than short-term speculation.

The familiar saying, “Failing to plan is planning to fail,” is particularly relevant when discussing retirement. Successful retirement planning rarely results from luck, market timing, or extraordinary investment decisions. Instead, it is generally built upon a series of sound decisions repeated consistently over many years.

As Warren Buffett reminds us:

“It is not necessary to do extraordinary things to get extraordinary results.”

The objective of this paper is also to provide context for understanding investment risk and risk-profile questionnaires. A "cautious" investor is not necessarily a cautious person in everyday life, nor is an "aggressive" investor necessarily reckless. Risk, within retirement planning, is best understood through the lens of time, objectives, and financial circumstances.

Understanding the stages of retirement planning provides a useful foundation for determining an appropriate risk profile and investment strategy.

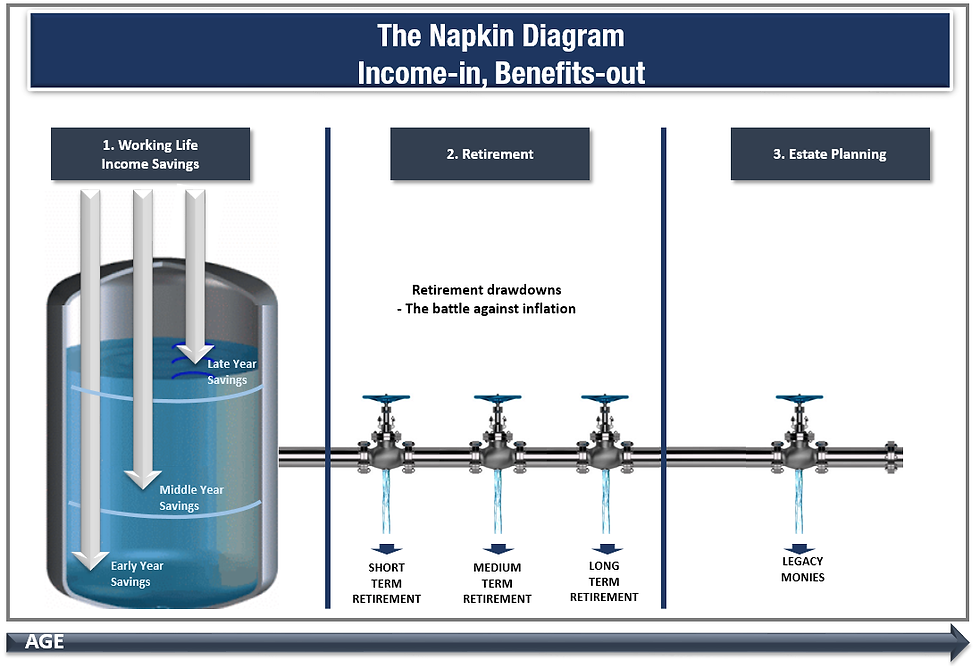

B. The flow of Money: Income In, Benefits Out

To keep retirement planning simple, we can view it through two diagrams- exploiting the theory that a good strategy should be visible on the back of a napkin, or the back of an envelope:

The Napkin: Income In, Benefits Out

The Envelope: The Phases of Retirement Planning

The first diagram illustrates a straightforward concept. During working life, savings accumulate into a retirement portfolio. In retirement, the process reverses and the portfolio provides income.

A successful retirement plan is one that creates sufficient assets to support a desired lifestyle when employment income is no longer required.

Part 1: Building the Retirement Pot

The retirement portfolio is simply a pool of assets accumulated throughout working life.

For most individuals, retirement planning begins when employment begins. Savings are generally funded from income, and as earnings increase over time, contributions often increase as well.

The principles are simple:

Consistent savings matter.

Time matters.

The more that is contributed over time, the greater the potential retirement assets available later.

This stage assumes a continuous flow of contributions during working life. Interruptions to saving may significantly reduce the eventual size of the retirement portfolio.

Part 2: Retirement and Drawdown

Retirement marks the transition from accumulating assets to drawing income from them.

Once employment income stops, the retirement portfolio becomes responsible for funding lifestyle expenses. At this stage, inflation becomes one of the greatest threats to long-term financial security.

Inflation measures the rising cost of goods and services over time. It is often described as a hidden tax because it steadily reduces purchasing power.

The Rule of 72 provides a useful way to estimate inflation's impact. By dividing 72 by the inflation rate, investors can estimate how long it takes for purchasing power to halve.

For example:

Inflation = 4%

72 ÷ 4 = 18

At a 4% inflation rate, purchasing power may be reduced by approximately half over 18 years.

The battle against inflation should begin long before retirement. A longer saving period provides more time for investments to grow and for retirement assets to outpace rising living costs.

Part 3: Estate Planning

No retirement plan can ignore life expectancy.

One theoretical measure of a perfectly efficient retirement plan would be for assets to be exhausted on the day of death after fully funding lifestyle requirements throughout retirement. However, most individuals prefer their assets to outlive them and provide benefits for future generations.

Estate planning therefore becomes an important component of retirement planning.

Life expectancy, inflation, investment performance, family circumstances, and unforeseen events all introduce uncertainty. These variables reinforce an important conclusion:

Retirement plans require regular review and adjustment.

Just as regular dental check-ups help maintain physical health, periodic financial reviews help maintain retirement health.

The complexity of financial products and investment solutions should never distract from the fundamental truth:

If contributions stop, growth potential is reduced. If contributions increase, the opportunity for future retirement income generally increases.

C. The stages of Retirement Planning

We divide retirement planning into four broad stages:

1. The Risk Period

2. Old Money vs. New Money

3. Pre-Retirement

4. Retirement

Each stage has different objectives and therefore different attitudes toward risk.

C1. Start with the End in Sight

It is useful to begin by considering retirement itself.

Even during retirement, individuals retain short-, medium-, and long-term needs.

Some assets may be required immediately to support lifestyle spending, while others may remain invested for many years. Retirement portfolios therefore often contain a mixture of:

Cash and short-term holdings

Moderate-growth investments

Long-term growth assets

The key question becomes:

How much cash is needed to support near-term lifestyle expenses?

This is a practical calculation influenced by living costs, health requirements, retirement goals, and personal preferences.

Although cash reserves may fund short-term spending, portfolios often still require growth assets to combat inflation and preserve purchasing power over longer periods.

Retirement therefore remains an exercise in balancing income needs with growth objectives.

C2. The Risk Period

The Risk Period generally occurs during the early stages of working life when retirement remains many decades away.

For younger investors with 30–40 years or more before retirement, short-term market fluctuations are often less important than long-term participation in growth assets.

During this stage, the primary focus is not portfolio value but asset accumulation.

Consider the example of a 25-year-old employee participating in a workplace savings scheme invested entirely in a broad equity market index.

At this stage, emphasis should often be placed on the number of investment units accumulated rather than on day-to-day portfolio values.

A market decline can actually benefit a long-term saver because ongoing contributions purchase more units at lower prices.

Viewed through this lens, volatility becomes less threatening and more opportunistic.

Historically, major equity market declines have been followed by recoveries. While the timing of recovery cannot be predicted, long-term investors benefit from allowing time to work in their favour.

This is why younger investors frequently maintain greater exposure to growth assets than investors approaching retirement.

The logic weakens progressively with age, particularly as retirement approaches and accumulated assets become more significant.

C.3 Old Money vs New Money

As retirement savings grow, risk takes on a different meaning.

Old Money: Protecting Accumulated Capital

The "old money" stage refers to assets that have already accumulated over many years.

Earlier in life, investors may focus primarily on growth. Later, protecting accumulated capital often becomes increasingly important.

One of the key concepts here is downside deviation.

Investment losses require larger gains to recover:

Market Decline | Gain Required to Recover |

10% | 11% |

20% | 25% |

30% | 43% |

50% | 100% |

As portfolios grow larger, many investors become more sensitive to these potential losses.

Some investors remain comfortable with equity-market volatility and continue to trust in the long-term tendency of markets to recover and grow. Others seek greater stability through diversification and reduced equity exposure.

Neither approach is inherently right or wrong; suitability depends on the individual's circumstances and risk tolerance.

A commonly repeated investment principle applies here:

Time in the market is generally more valuable than timing the market.

Trying to predict market peaks and troughs consistently is extremely difficult, even for experienced investors.

New Money: Continuing the Growth Journey

While accumulated assets may require greater protection, new contributions represent fresh capital.

These new savings still have a long investment horizon and may remain suitable for growth-oriented investments.

This creates an opportunity for investors to adopt different strategies for different portions of their portfolio:

· Protect accumulated assets where appropriate.

· Continue seeking long-term growth with new contributions.

This approach can provide a balance between capital preservation and continued asset growth.

C.4 Pre-Retirement

The pre-retirement stage focuses on preparing the retirement portfolio for income generation.

The key question becomes:

How much money will be required during the first few years of retirement?

Retirement often introduces new expenses:

Healthcare costs

Travel plans

Lifestyle goals

Major purchases

These objectives usually require readily accessible capital.

At this stage, the retirement portfolio begins transitioning toward its final structure:

Short-term assets for immediate spending needs

Medium-term assets for stability and moderate growth

Long-term assets for inflation protection

Determining appropriate allocations is partly science and partly judgment. Financial planning tools can assist, but personal circumstances ultimately drive the outcome.

The closer retirement approaches, the more important it becomes to align the portfolio with anticipated income requirements.

D. Summary: Simplicity Through Managing Complexity

Retirement planning involves many variables:

Inflation

Investment returns

Longevity

Health

Employment circumstances

Taxation

Family considerations

Risk profiling helps simplify these complexities by matching investment strategies to individual circumstances.

Risk profiles should not be viewed as permanent labels. They often evolve as people gain experience, increase investment knowledge, and move through different stages of life.

Most risk assessments consider factors such as:

Investment knowledge

Investment experience

Time horizon

Tolerance for volatility

Tolerance for capital loss

For purposes of this paper, we use five broad categories.

D1. Defensive / Guarantee

The Defensive profile suits highly cautious investors, first-time investors, or those with short investment horizons.

The primary objective is capital preservation.

Typical holdings include:

Cash

Cash equivalents

Government bonds

Guaranteed products

Key Characteristics

Suitable for investment horizons of up to three years, potentially five.

Appropriate for highly risk-averse investors.

May suit default retirement options for passive participants.

Minimal volatility.

Primary Risk

The greatest risk is failing to keep pace with inflation, resulting in declining purchasing power over time.

D2. Cautious

The Cautious profile suits investors willing to accept limited risk in pursuit of modest growth.

These investors seek stability while aiming to modestly exceed inflation.

Typical allocations include:

Significant holdings in cash and bonds

Limited exposure to equities and growth assets

Key Characteristics

Low probability of long-term capital loss.

Some short-term volatility.

Focus on preserving purchasing power.

Common Applications

Pre-retirement portfolios.

Retirement income reserves.

Investors expecting major future financial changes.

D3. Balanced

Balanced investors seek a compromise between growth and capital preservation.

They are willing to accept some volatility while maintaining an emphasis on diversification.

Typical balanced portfolios contain a mix of:

Growth assets

Defensive assets

Often in roughly equal proportions.

Key Characteristics

Moderate volatility.

Reasonable growth potential.

Strong diversification.

Common Applications

Medium-term retirement assets.

Managing accumulated capital while maintaining growth potential.

D4. Growth

Growth investors prioritise long-term capital appreciation.

They generally understand and accept market volatility in exchange for higher expected returns.

Portfolios typically hold a majority allocation to equities and other growth assets.

Key Characteristics

Significant short- and medium-term volatility.

Strong potential for long-term growth.

Suitable for long investment horizons.

Common Applications

The Risk Period.

Investors seeking to improve purchasing power and outpace inflation over time.

D5. Aggressive

Aggressive investors seek maximum long-term growth and are comfortable with substantial market fluctuations.

Portfolios are heavily invested in equities and may include concentrated themes, sectors, or regional exposures.

Key Characteristics

High volatility.

Significant upside potential.

Greater exposure to specific market risks.

Common Applications

Additional Voluntary Contributions (AVCs).

Specialist investment themes.

Investors willing to maintain substantial growth exposure into retirement.

It is important to remember that portfolio values fluctuate. Market declines do not become actual losses until assets are sold.

Probability Analysis and Ongoing Management

Retirement forecasts rely on assumptions about future returns, inflation, longevity, and spending patterns. No calculator can predict the future with certainty.

For this reason, retirement planning should be viewed as an ongoing process rather than a one-time event.

Regular reviews allow investors to assess:

Whether savings levels remain sufficient.

Whether risk tolerance has changed.

Whether investment allocations remain appropriate.

Whether retirement objectives remain achievable.

Monte Carlo analysis and other probability-based tools can help investors evaluate a range of possible outcomes rather than relying on a single forecast.

While these tools are imperfect, they become increasingly useful when used consistently over time.

Ultimately, the purpose of retirement planning is not to predict the future with precision but to prepare for uncertainty with discipline and flexibility.

Conclusion

Retirement planning can appear complex because it involves countless variables. Yet the underlying principles are remarkably simple.

Save consistently. Invest thoughtfully. Understand your risk tolerance. Review your progress regularly.

No one can control inflation, market cycles, or life expectancy. However, we can control our savings habits, investment decisions, and commitment to long-term planning.

A successful retirement is rarely the result of perfect forecasts or market timing. More often, it is the product of consistent decisions made over many years.

Ultimately, retirement planning is about taking control of the factors you can influence and adapting to those you cannot. In that sense, the path to retirement success is not complexity - it is disciplined simplicity.

Comments